There must be a map or model of the data, which shows the zone to be navigated and upon which is marked the best route.

David Foster, Ph.D.

It’s very useful to believe that if several people can do something well, then the skill can be copied, or modeled, and taught to someone else. This belief is what neuro-linguistic programming (NLP), or the science of modeling, is all about. To develop a good model, you need to find several people who can do what you are modeling well. You then need to interview those people to find out what they do in common. These are the key tasks involved in making the model. It’s very important to find out what they do in common. If you don’t, you’ll simply discover the idiosyncrasies of the people involved, which usually are not that important.

I’ve worked with hundreds of outstanding traders and investors in a coaching role over the past 25 years. During that time, I’ve had the opportunity to learn how to conduct trading research from these experts. The steps are quite clear and easy to do. This chapter is a synopsis of the model I’ve developed through these associations. In addition, we’ve improved the model since the last edition of this book.

1. Take an Inventory

The first key step is to take an inventory of yourself – your strengths and weaknesses. To have market success, you must develop a system that is right for you. In order to develop such a system, you must take a careful self-inventory – of your skills, your temperament, your time, your resources, your strengths, and your weaknesses. Without taking such an inventory, you cannot possibly develop a methodology that’s right for you.

Among the questions you need to consider:

- Do you have strong computer skills? If not, then do you have the resources to hire someone who does or who can help you to become computer proficient?

- How much capital do you have? How much of that is risk capital? You must have enough money to trade or invest with the system you develop. Lack of sufficient funds is a major problem for many traders and investors. If you don’t have sufficient funds, then you cannot practice adequate position sizing. This is one of the essential ingredients to a successful system that most people ignore.

- How well can you tolerate losses?

- How are your math skills? And what’s your level of understanding of statistics and probability?

There are many important issues that you should contemplate. For example, consider what time constraints you have. If you have a full-time job, think about using a long-term system that requires you to spend only about half-hour each night looking at end-of-day data. Stop orders are then given to your broker for the next day. Trading such a system doesn’t take much time, so it’s quite appropriate to use if you don’t have much time. In fact, many professionals who spend all day with the markets still rely on long-term systems that use only end-of-day data.

Let’s look at another issue you should consider. Are you looking to be in the market with your own money or someone else’s? When you trade for other people, you have to deal with the impact of their psychology on your trading, which could be quite substantial. For example, what would your trading be like if you had to deal with clients who were always complaining to you about something?

Say you are a money manager, and after two losing months, your client withdraws her money. You then have three winning months, and the client decides to reinvest with you. After you have another two losing months, she again withdraws. She decides to wait until you get really hot in the markets and after five winning months, she puts her money back in .You have again, two losing months. The result of all this is a client who is continually losing while you, as a money manager, have made a lot of money. But the wear and tear that she will have experienced could also affect you and your trading, especially if she complains a lot.

I’d also recommend that you take a thorough inventory of your personal psychology. You should spend a lot of time thinking about the questions asked in the self-inventory in Chapter 3 on managing client money and think about your answers. Did you just give a quick answer, or did you given an accurate assessment of what you believe and feel? In addition, did you just answer the questions, or did you put a lot of thought into each answer before you put it down on paper? Compare your answers with Tom Basso’s answers so that you can compare yourself with a top professional money manager.

In addition to the questions in Chapter 3, as part of the self-inventory you do, ask yourself the very important question, “Who am I?” The answer to that question is the basis for everything else you do, so think about it seriously.

For example, I’ve been working with a large trading firm, and early in 2006 the president of the firm cancelled his monthly consulting call with me. He said he was changing what he was doing and needed to sort out some important thins in his mind. Well, after reading his e-mail, it was clear to me that he was readdressing the question “Who am I?” In this particular case, he had been (1) the CEO of the company, (2) the head of a trading group, and (3) one of the best traders in the group. The answer he arrived at led him ultimately to disband his trading group to focus more on his own trading because his self-inventory helped him decide that role number 2 did not suit him.

To adequately answer the “Who am I?” question, I would strongly suggest that you write down all of your beliefs about yourself. Sit down with several sheets of paper and start writing free-flowing notes about yourself. Who are you really and what do you believe? When you’ve written down about 100 beliefs, you’ll have a pretty good idea.

Here are a few of the beliefs one of my clients wrote down:

- I’m a full-time professional who has several hours each day to commit to being the best trader I can be.

- I am totally committed to becoming a full-time trader within the next 12 months.

- I am a short-term trader for my personal account and a very long-term trader for my retirement account.

- I believe I can make 50 percent or better in my short-term trading account, while I’m only trying to outperform the market in my retirement account.

Those are just a few of the beliefs about himself that he wrote, but hopefully you can begin to see from them how they shape everything else. Now it’s time for you to write down your beliefs about yourself.

2. Develop an Open Mind and Gather Market Information

One of the three-day workshops that we conduct is called Developing a Winning System That Fits You. And we also have an audio series on that topic from a prior workshop. Most people learn a great deal from that workshop or audio series, but sometimes people don’t learn enough until they’ve addressed some of their psychological issues first. For example, some people seem totally closed to what we are trying to teach. They have their own ideas about what they want, and they are just not open to a general model for improving their methodology – much less to specific suggestions on how they should change. And the interesting thing is that the people who are most closed to the ideas presented are usually people who need the material the most.

Thus, the first part of step 2 in the system development model is to develop a completely open mind. Here are some suggestions for doing that.

First, you need to understand that just about everything you’ve ever been taught – including every sentence you’ve read so far in this book – consists of beliefs. “The world is flat” is a belief, just as the statement “The world is round.” You might say, “No, the second statement is a fact.” Perhaps, but it is also a belief – with a lot of important meaning in each word. For example, what does round mean? Or for that matter, what does world mean?

Anything that seems to be a fact is still relative and depends upon the semantics of the situation. Its factually depends on some assumptions you are making and the perspective you are bringing to the situation – all of which are also beliefs. You’ll become a lot less rigid and much more flexible and open in your thinking if you consider “facts” to be “useful beliefs” that you’ve made up.

The reality that we know consists solely of our beliefs. A soon as you change your beliefs, then your reality will change. Of course, what I’ve just said is also a belief. However, when you adopt this belief for yourself, you can begin to admit that you don’t really know what is real. Instead, you just have a model of the world by which you live your life. As a result, you can evaluate each new belief in terms of its “utility.” When something conflicts with what you know or believe, think of yourself, “Is there any chance that this is a more useful belief?” You’d be surprised at how open you’ll suddenly become to new ideas and new input. One of my favorite quotations is the following from Einstein: “The real nature of things, we shall never know, never.”

Keep in mind the following: You don’t trade or invest in markets – you trade or invest according to your beliefs about the markets.

Thus, part of the necessity of having an open mind is the requirement to determine just your beliefs about the market. When you are not open, they don’t seem like “beliefs” – they just seem like “what is”. Trading “an illusion”, which everyone does, is particularly dangerous when you don’t know it. And you may be deluding yourself extensively with your beliefs.

Charles LeBeau, a veteran trader of 40 years, says that when he started to design trading systems for the computer, he had hundreds of beliefs about the market. Most of those beliefs did not stand up to the rigors of computerized testing.

When your mind is open, start reading about the markets. I strongly recommend almost any book written by Jack Schwager. However, start with Market Wizards and The New Market Wizards. They are two of the best books available on trading and investing. Two other books by Schwager, Fundamental Analysis and Technical Analysis, are also excellent.

Computer Analysis of the Futures Market, by Charles LeBeau and David Lucas, is one of the best books available on the systematic process of developing a trading system. Indeed, I’ve learned a lot from reading that book and from conducting regular workshops with Chuck. I’d also recommend Perry Kaufman’s book Smarter Trading; Cynthia Kase’s book Trading with the Odds; and William O’Neil’s book How to Make Money in Stocks. Tushar Chande’s book Beyond Technical Analysis is also good in that it gets the reader to think about concepts that are beyond the scope of this volume.

The suggested readings will give you the appropriate background required to develop useful beliefs about the markets that will support you in the game ahead of you. They will answer a lot of the pressing questions about trading that might be cluttering your mind. More detailed information about these books is provided in the Recommended Readings at the end of this book.

Once you’ve completed this reading list, write down your beliefs about the market. Every sentence in this book represents one or more of my beliefs. You may want to find the ones you agree with having to do with the market. They will be a good starting point for your task of finding your beliefs about the market. This step will prepare you for subsequent tasks you will have to tackle in exploring the markets and developing your own system for making a lot of money. This study of the markets you will have done and the list of your beliefs that you study will have generated (you should write down at least 100 of them) will probably become the basis for a trading system that fits you. At the very least, your list will make a good starting point. Look at each part of a trading system, as described in this book, and make sure that you’ve listed your beliefs about each of them.

As you read this book, make a note of what you agree with and what you disagree with. There is no right or wrong, just beliefs and the meaning and amount of energy you attach to them. Doing this exercise will tell you a lot about your beliefs. For example, I gave a manuscript of this book to ten traders for their comments. What I got back simply reflected their beliefs. Here are some examples:

- I would argue that position sizing is part of your system, not a separate system.

- Indicators are not distortions of chart data but rather derivations.

- There are a lot of flaws in expectancy because of judgmental heuristics such as “curve fitting,” data mining,” and the long-term data problem.

- I don’t believe that catastrophic events are predictive except that they might increase or decrease market volatility and/or value. Thus, designing a system that adapts to changing volatility is the key.

- A bad trade is not a losing trade, but one which didn’t meet my entry criteria that I took anyway.

- I don’t believe that reliability (win rate) has anything to do with your entry. Instead, it has to do with your exits.

- When you say we’re in a secular bear market, you will create a psychological bias for your readers. You don’t have a crystal ball.

- You say the markets move sideways 85 percent of the time. I think the estimate is high – it’s probably 50 to 75 percent of the time.

The people with these beliefs each wanted me to make changes in the book to reflect their beliefs. Instead, I chose to keep my beliefs and just inform you that you might have beliefs that conflict with mine. Just make sure that your belief is useful for you. What’s really important is to recognize your beliefs because you will only trade a system that fits your beliefs.

3. Determine Your Mission and Your Objectives

You cannot develop an adequate system or making money in the market unless you totally understand what you are trying to accomplish in the markets. Thinking about your objectives and getting them clearly in mind should be a major priority in your system development. In fact, it probably should occupy 20 to 50 percent of your time in designing a system. Unfortunately, most people totally ignore this task or just spend a few minutes doing it. To see if you’re spending adequate attention on determining your objectives, start by recalling how much time you spent working on the exercise in Chapter 3.

Give Chapter 3 a lot of time nd a lot of thought. The chapter contains a detailed questionnaire for you to fill out. If you took only 15 to 30 minutes to answer the same questions I asked Tom Basso, then you are probably not doing an adequate job. Establishing objectives is one of the tasks that most people want to avoid, but if you want to develop a great system for trading or investing, then you must give this task sufficient attention. Remember how important it is to keep an open mind? Doing an adequate job with your objectives is part of being open.

4. Determine The Concept That You Want to Trade

In my experience as a trading coach, only certain concepts work. So your next step is to familiarize yourself with the various concepts that work and decide which of them you wish to focus on. I’ve devoted an entire chapter to explaining these concepts, but I’ll briefly outline them here.

Trend Following

This concept assumes that markets, at times, tend to trend (that is, they move up or down for a fairly long period of time). If you can spot when the trend starts and capture much of the move, then you can make a lot of money as a trader. However, to be a trend follower, you must be able to buy what’s going up and sell what’s going down. And if it’s been going up for a while, so much the better – you still must be able to buy it if you want to trade this particular concept. However, all trend followers must ask themselves the following questions:

- How will I spot my trends? How will I know a market is trending?

- Will I be trading trends on the upside and the downside?

- What will I do when the market goes sideways (which tends to be about 85 percent of the time, according to my estimates)?

- What will my entry criteria be?

- How will I handle corrections?

- How will I know when the trend is over?

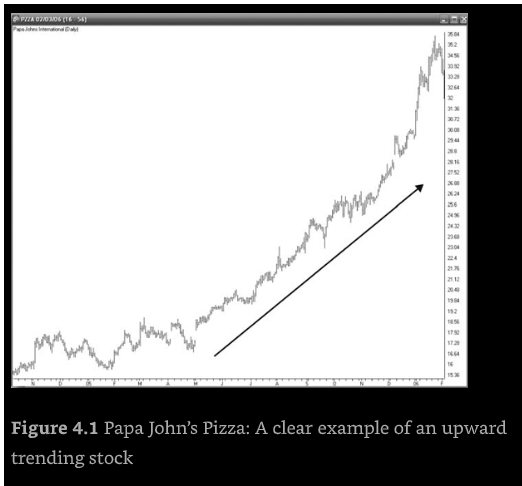

Figure 4.1 shows a great example of a trend. You can see that if you can spot such trends early enough, you have a tremendous potential for making a lot of money. Tom Basso does an excellent job of describing trend following as a concept in Chapter 5.

Band Trading

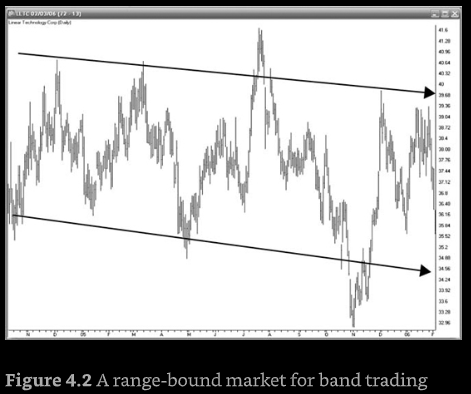

The second concept that people can successfully trade is band trading. Here we make the assumption that the markets we are trading are somewhat range bound. Such markets go up for a limited period of time until they reach he top of the range. These markets then turn down for a limited period of time until they reach the bottom of the range. Figure 4.2 shows an example of a range-bound market that you could use to trade bands.

Notice that in the particular instance of the stock selected, Linear Technology Corp,, you could do quite well selling whenever the price touched and then penetrated the upper band. Similarly, you could do quite well buying whenever the price touched and then penetrated the lower band. However, the common issues always arise. How do you determine the bands? I just drew them in after the fact, but there are mathematical formulas to make them more objective. How do you close out a position, especially since the price does not always touch the opposite band? And what if the band you are using breaks down?

If you can spot such a range-bound market, then your objective would be to sell at the top of the range and buy at the bottom of the range. And if you like this particular concept, then the primary questions you must ask yourself are the following:

- How do I find range-bound markets to buy?

- Will my bands work in a trending market>

- How do I define the range? For example, should I use fixed or static bands?

- What are my entry criteria?

- What if my band breaks down? How will I exit?

- Do I exit at the other end of the band and under what criteria?

D.R. Barton does an excellent job of discussing band trading in Chapter 5.

Value Trading

Value Trading centers on some definition of value. You buy stocks or commodities that are undervalued and sell them when they are overvalued. When you adopt this approach, the key questions you must ask yourself are the following:

- How do I define value?

- When is something undervalued?

- What are my criteria for buying something that is undervalued?

- What are my criteria for selling something that is overvalued?

Many fundamentalists and portfolio managers use some form of value trading.

Arbitrage

Arbitrage occurs when you are able to buy something at a low price in one place and sell it for a higher price in some other place. These discrepancies usually occur because of some temporary loophole in the law or in the way the marketplace works. For example, one of my clients recently discovered that you could buy a seat on the Chicago Board of Trade (CBOT) for about $3 million, but he could sell the various components of the seat for $3.8 million. That’s a 27 percent built-in profit on each transaction. It’s an easy surefire trade. However, easy trades usually have their downfall. In this case, to purchase the Chicago Board of Trade seat required that he also purchase Chicago Board of Trade stock. He was required to keep the stock six months before selling it. Thus, if the stock were to drop 27 percent during the six months he was required to hold it, then it would negate all of his profits. Thus, like most arbitrage trades, there is some risk.

The key questions you must ask yourself when arbitrage is your niche are the following:

- What areas of the market do I need to search to find loopholes?

- What exactly is the loophole, and how can I best take advantage of it?

- What are the risks?

- How long will the loophole last, and how will I know it’s over?

Many floor traders, especially those using options, conduct various forms of arbitrage. In addition, the few day traders who have survived since 2000 have survived by finding good arbitrage situations. The late Ray Kelly does an excellent job of discussing arbitrage in his section of Chapter 5.

Spreading as a Concept

Another technique used by market makers and options traders is spreading. Spreading is somewhat related to arbitrage in that it requires that you usually buy one thing and sell something else, hoping you have the relationship right. For example, most trading of foreign currency is a form of spreading because you become long (that is, you own it and profit if it goes up) in one currency against another (that is, you profit if it goes down).

The key questions you must ask yourself as a spreader are the following:

- What do I think might move?

- What can I short against that move to hedge my risk?

- Is there a limit to my profit (as there is with some options spreads)?

- How ill I know if I’m wrong?

- Or if I’m right, how will I know the move is over?

Kevin Thomas ,the first person to join my Super Trader program, writes about spreading in Chapter 5.

Other concepts included in Chapter 5 that you might also select from are seasonals (taking trades at some particular time period that is most appropriate for a market move) and deciding that there is some secret order to the universe. I don’t know of any other trading concepts besides these, but this is still a wide range of concepts from which you can select one or two.

5. Determine The Big Picture

I’ve been coaching traders since 1982, and during this time I’ve seen many market cycles. When I first started coaching, most of my traders were futures traders and options traders. This was interesting considering that I was starting right at the beginning of the huge secular bull market in stocks.

During the 1980s most of my clients continued to be futures traders, although the futures markets tended to be dominated by big CTAs. And then trends in futures toward the end of the decade (as inflation quieted) tended to be small. And I noticed that, gradually, all of these traders were moving toward trading foreign exchange.

Later, in the mid-1990s, I started to get a lot of equity traders as clients. This peaked in March 2000 when over 70 people attended our Stock Market Workshop. At that time, one bartender in the local hotel where we were giving such workshops remarked, “Perhaps we should attend Dr. Tharp’s stock market workshop.” However, the other bartender responded, “No, I could teach that workshop.”

Such things usually happen at market extremes, and you know what happened in 2000. Now, in 2006, I’m finding that about half of our clients are again futures traders. So our clients clearly move in cycles, gravitating toward the hot market – perhaps at the wrong time. As a result, I now think it’s critical to make part of your system development an assessment of the big picture. Several non-correlated systems that fit the big picture would make up a great trading business plan. In addition, you might develop more systems to use should the big picture change.

I believe that this step is critical, so I’ve developed a new chapter in this book to helping you assess the big picture. In addition, I write a monthly update on the big picture in my free e-mail newsletter Tharp’s Thoughts.

6. Determine your time frame for trading

Your sixth task to decide how active you want to be in the market. What is your time frame for trading? Do you want to have a very long-term outlook, probably making a change in your portfolio only once a quarter? Do you want to be a stock trader who holds positions for a year or longer? Do you want to be long-term futures trader whose positions last one to six months? Do you want to be a swing trader who might make several trades each day with none lasting more than a few days? Or do you want the ultimate in action – being a day trader who makes 3 to 10 trades each day that are closed by the end of the day so that you have no overnight risk?

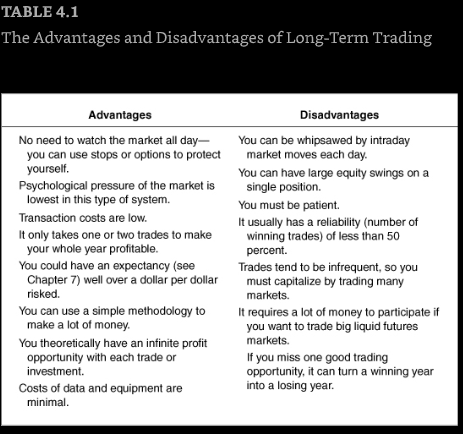

Table 4.1 shows the advantages and disadvantages of long-term trading. Long-term trading or investing is simple. It requires little time each day and has minimal psychological pressures each day – especially if you take advantage of your free time to work or spend time with your hobbies. You can typically use a fairly simple system and still make a lot of money if you adequately size your positions.

I think the primary advantage of long-term trading or investing is that you have an infinite profit opportunity (theoretically at least) on each position in the market. When you study many of the people who’ve gotten rich through investments, you’ll find that in many instances wealth builds up because people have bought any stocks and just held on to them. One of the stocks turns out to be a gold mine – turning an investment of a few thousand dollars into millions over a 10 to 20 year period.

The primary disadvantage of long-term trading or investing is that you must be patient. For example, you might not get a lot of opportunities, so you must wait for them to come along. In addition, once you’re in a position, you must go through fairly extensive equity swings (although you can design something that minimizes them) and have the patience to wait them out. Another disadvantage of longer-term trading is that you generally need more money to participate. If you don’t have enough money, then you cannot adequately size your positions in a portfolio. In fact, many people lose money in the markets simply because they don’t have enough money to participate the type of trading or investing that they are doing.

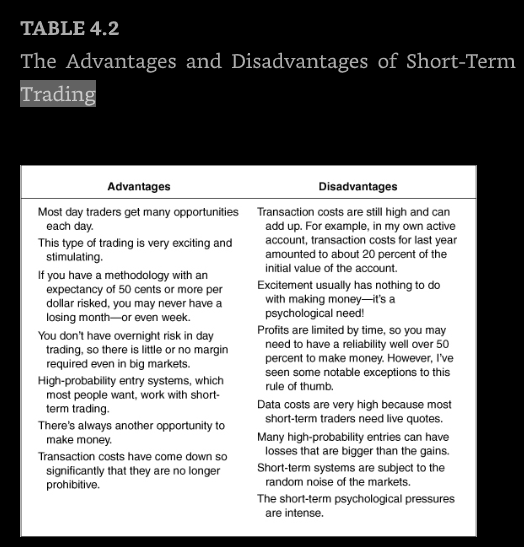

Shorter-term trading (which might be anything from day trading to swing trading of one to five days ) has different advantages and disadvantages. These are illustrated in Table 4.2. Read through the list and then compare it with the long-term table. Once you’ve done so, you can then decide for yourself what best fits your personality.

I once met a short-term foreign-exchange trader who made about six trades a day. No trade would last more than a day or two. However, the fascinating thing about what he was doing was that his gains and losses were about equal and he made on 75 percent of his trades. This is a fascinating trading methodology. He had $500,000 to trade with and a $10 million credit line with a bank. When you understand position sizing, as discussed later in this book, you’ll realize that this system comes as close to the Holy Grail as anything in existence. He could easily make a hundred million each year with that system and the capital he has.

However, that’s not the case with most short-term systems. Most of them seldom have a reliability much higher than 60 percent, and their gains are usually smaller than their losses – sometimes even leading to a negative expectancy. Sometimes one big loss can ruin the whole system and psychologically devastate the trader. In addition, the psychological pressures of short-term trading are intense. I’ve had people call me who say something like this:

I make money almost every day, and I haven’t had a losing streak in almost two years. At least until now. Yesterday, I gave back all the profits I had made over the last two years.

Keep that in mind before you decide that short-term trading is for you. Your profits are limited. Your transaction costs are high. Most importantly, the psychological pressures could destroy you. Nevertheless, my belief is that the largest profit percentages are made by active short-term traders who really have their psychology together. I’ve seen short-term traders who could make as much as 50 percent or more per month (on small amounts of money such as $50,000 account) when they were very in tune with the market and themselves.

7. Determine the essence of your trading and how can you objectively measure it

What is the key idea that you’ve observed? The first part of your idea should tell you the conditions under which the move occurs. How can you objectively measure that part of the idea? Typically, your answer to this question will give you two elements of your system: the setup conditions that you might want to use and the timing or entry signal. These topics are discussed extensively later in this book.

Your step and timing signal are important for the reliability of your system – how often will you make money when such a move occurs? This should be tested independently from all of the other components of your system.

LeBeau and Lucas in their book, cited earlier, have an excellent method for testing such signals. What they do is determine the reliability (that is, the percentage of time it is profitable) of the signal after various time periods. You might try an hour, the end of the day, and after 1,2,5,10 and 20 days. A random system should give you an average reliability of about 50 percent (that is, generally between 45 to 55 percent). If your concept is any better than random, then it should give you a reliability of 55 percent or better – especially in the 1- to 5-day time periods. If it doesn’t do that, then it is no better than random, no matter how sound the concept seems to be.

When you do your entry testing, if entry reliability is your objective, then the only thing you are looking at is how often it is profitable after the selected time periods. You have no stops, so that is not a consideration. When you add stops, the reliability of your system will go down because some of your profitable trades will probably be stopped out at a loss. You also do not consider transaction costs (that is, slippage and commissions) in determining its reliability. As soon as you add transaction costs, your reliability will go down. You want to know that the reliability of your entry is significantly better than chance before these elements are added.

Some ideas seem so different when you first observe them. You might find that you have a hundred examples of great moves. Your idea is common to all of them. As a result, you get very excited about it. However, you also must consider the false-positive rate. How often is your idea present when there is not a good move? If the false-positive rate is very high, then you don’t have a great concept, and it might not be much better than chance.

One precaution you should keep in mind in using this kind of testing is that reliability is not the only consideration in your system. If your entry idea helps you capture giant moves, then it may be valuable.

Some people would argue that I’ve neglected an important step in system development: optimization. However, optimization really amounts to fitting your idea to the past. The more you do this, the less likely your system is to work in the future. Instead, I believe that you should work toward understanding your idea as much as possible. The more you understand the real nature of your edge, the less historical testing you will have to do.

I believe that you should work toward understanding your idea as much as possible. The more you understand the real nature of your edge, the less historical testing you will have to do.

8. Determine what your initial 1R risk will be

An important part of your idea is to know when it is not working. Thus, the next step is to understand the effect of adding a protective stop. Your protective stop is that part of your system that tells you when to get out of a trade in order to protect your capital. It is a key portion of any system. It’s that point at which you should get out in order to preserve capital because your idea doesn’t seem to to be working. The way you’ll know your idea is not working depends upon the nature of your idea.

For example, suppose you have some theory that says there is “perfect” order to the market. You can pinpoint market turning points to the day – sometimes to the hour. In this case, your concept would give you a setup that is the time at which the market is supposed to move. Your entry signal should be a price confirmation that the market is indeed moving, such as a volatility breakout (as discussed in Chapter 9). At this point, you need a stop to tell you that your idea isn’t working. What might you select? What if the market exited the time window without your making a significant profit? Then you’d probably want to get out because you didn’t predict the turning point that was the reason for your entry. Or you might consider the average daily price range (such as the average true range) of the last 10 days to be the amount of noise in the market. If the price moved against you by that amount (or some multiple of that amount), you might want to get out.

Examples of protective stops are discussed extensively in Chapter 10. Read that chapter in detail, and pick one (or more) that best fits your idea. Or perhaps your idea leads to a logical stop point that isn’t discussed in that chapter. If so, then use that logical stop point.

Think about what you are trying to accomplish with your entry. Is it fairly arbitrary? Do you think a major trend should be starting? If so, then you’ll probably want to give the market lots of room so that the trend will develop. Thus, you’ll want to use a very wide stop.

On the other hand, perhaps your idea is very precise. You expect to be wrong a lot, but when you are right, you don’t expect to lose money on the trade. If that is the case, then you can have very close stops that don’t lose much money when they are executed.

Once you’ve decided on the nature of your stop, add your stop plus transaction fees (that is, estimated slippage and commissions) to the calculations you did in the previous step and redo them. You’ll probably find a significant drop in the reliability of your entry signal when you add in these percent, it will probably drop to 50 to 55 percent when you add your stop and the transaction costs to each trade.

At this stage of the process you’ve now determined what your initial risk, or R, will be for ever trade you make. This is a huge step for you because you can now think of your profits as some multiple of your initial risk (or R multiples). For example, most good traders believe they should never take a trade unless it gives them a potential reward that is at least three times the size of their potential risk (3R). You’ll learn later in this book that every system is really defined by the R-multiple distribution of the profits and losses it generates.

9. Add your profit-taking exits and determine the R-multiple distribution of your system and its expectancy

The third part of your system should tell you when the move is over. As a result, the next step is to determine how you will take your profits. Exits are discussed extensively in Chapter 11, where you’ll learn about what exits are most effective. Read through that chapter and determine what exits best fit your concept. Think about your personal situation – what you’re trying to accomplish, your time frame for trading, and your idea – before you select your exit.

Generally, if you’re a long-term trader or investor who is trying to capture a major trend or enjoy the reward of long-term fundamental values, then you want a fairly wide stop. You don’t want to be in an out of the market all the time if you can help it. You’ll only make money on 30 to 50 percent of your positions, so you want your gains to be really big – as much as 20 times your average risk. If this is the case, your exits should be designed to capture some big profits.

On the other hand, if you are a day trader or scalper who is in and out quickly, the you’ll want fairly tight stops. You expect to be right on better than 50 percent of your positions – in fact, you must be because you are not in the market long enough for huge rewards. Instead, you’re looking for small losses with a reward-to-risk ratio of about 1. However, it is possible to make money 50 to 60 percent of the time, have your losses at minimal levels, and still capture a few trades that will give you big profits.

Overall what you are looking for when you add in your exits is to make the expectancy on your system as high as possible. Expectancy is the mean R multiple of your trading system. Or stated another way, it’s the average amount of money you’ll make in your system per trade – over many, many trades – per dollar risked. The exact formula for expectancy, plus the factors that go into it, are discussed extensively in Chapter 7. At this point in the model , however, your goal is simply to produce as high an expectancy as possible. You are also looking for as much opportunity as possible to trade (within a limited time frame) to realize that expectancy.

In my opinion, expectancy is controlled by your exits. Thus, the best systems have three or four different exits. You’ll need to test the ones you select one at a time. You’ll probably want to select them logically, based on your trading and/or investing idea. However, you’ll want to test them with everything in place (up to this point) to determine what they do to your expectancy.

Once you determine your expectancy, look at your system results trade by trade. What is the makeup of the expectancy? Is it mostly made up of a lot of 1:1 or 2:1 reward-to-risk ratio trades? Or do you find that one or two really big trades make up most of the expectancy? If it’s long term and you don’t have enough contribution from big trades, then you probably need to modify your exits so that you can capture some of those big trades.

10. Determine the accuracy of your R-multiple distribution

At this point you have the essence of a trading system because you should be able to determine the R-multiple distribution of that system. In other words, look at all of your historical profit and loss results. What does that distribution look like? Are your losses 1R or less, or do you tend to have losses that are bigger then 1R? What do your profits look like as a function of your initial risk? Do you have some occasional 20R trades? Or even 30R trades? Or do you have many 2R and 3R gains? What’s the nature of the R-multiple distribution that you’ve produced?

You might have a lot of biases that influence your initial determination of your expectancy. As a result, you now need to determine the accuracy of your R-multiple distribution by trading it in real time with a very small size. What if you traded with 1 to 10 shares of stock or a single commodity contract? What kind of R-multiple distribution would you get doing that? Is it similar to the one you worked out theoretically or through historical testing? Does it have a good expectancy?

You also need to know what kind of R-multiple distribution your trading system produces in each kind of market. For example, markets can go up, down, or sideways. They can do so quietly or in a volatile manner. If you combine those elements, we now have six different types of markets:

- Up quiet

- Up volatile

- Sideways quiet

- Sideways and volatile

- Down quiet

- Down volatile

You should know what to expect from your system in each of those types of markets. And this means a minimum of 30R multiples from completed trades from each of those markets. And if you don’t have that kind of data, then at least need a theoretical understanding of how your system will perform in each of those markets before you begin trading. Will your system work in down volatile markets? Most systems, except for a few options systems, will not work in sideways, quiet markets. But you need to know that for sure.

11. Evaluate your overall system

Once you have a system, you need to determine how good it is. There are several ways you can do that.

The most naïve way to determine how good your system may be is through its win rate. Here you’d decide that the system that wins most of the time will be the best system. However, in Chapter 1 on judgmental biases, we’ve already shown that you could have a system that’s right 90 percent of the time and still lose money if you trade it enough. Thus, the win rate is not the best measure.

There are much better methods you can use to determine the quality of your system:

- The expectancy of the system. Isn’t a system that produces an average gain of 2.3R per trade better than a system that produces an average gain of only 0.4R? Well, the answer is “Sometimes.”

- How about the expected gain in terms of R at the end of a fixed time period? What if system 1 produces 20R in gains at the end of the month while system 2 produces 30R? Isn’t system 2 better ? Again the answer is “Sometimes” because it also depends on the variability of your system. For example, the system that produces an average gain of 30R might have a negative expectancy 30 percent of the time, while the system that produces an average gain of 20R might never have a negative expectancy.

Once you determine the accuracy of your system, and you know how it will perform in various kinds of markets and how it will perform compared with other possible systems, then it is time to work on meeting our objectives. And the way you will meet your objectives is through position sizing.

12. Use Position Sizing to meet your objectives

Your expectancy is a rough estimate of the true potential of your system. Once you develop an adequate system, then you need to determine what algorithm you will use to size your positions. Position sizing is the most important part of any system because it is through position sizing that you will meet your objectives or meet ruin. Position sizing is that part of your system that helps you meet your objectives.

How much size will you put on in any one position? Can you afford to even take a single position (that is, one share of stock or one futures contract)? These questions are keys to being able to achieve your objectives – whether you desire a triple-digit rate of return or a smooth equity curve. If your position sizing algorithm is inappropriate, you will go bust no matter how you define “going bust” (whether it’s losing 50 percent of your capital or all of it). But if your position-sizing techniques are well designed for your capital, your system, and your objectives, then you can generally meet your objectives.

Position sizing is the most important part of any system because it is through position sizing that you will meet your objectives or meet ruin. Position sizing is that part of your system that helps you meet your objectives.

Chapter 14 of this book discusses a number of position-sizing models that you may want to consider in the design of your system. Once you have defined your objectives and developed a high-expectancy system, you can use these models to accomplish your objectives. However, you need to apply and test various position-sizing models until you find something that perfectly fits what you want to accomplish.

13. Determine how you can improve your system

The next task in developing your system is to determine how you can improve it. Market research is an ongoing process. Markets tend to change according to the character of the people who are playing them. For example, right now the stock market is dominated by professional mutual fund managers. However, of the 7,000 plus managers, fewer than 10 of them have been around long enough to have seen the prolonged bear markets that occurred in the 1970s. In addition, the futures market is dominated by professional CTAs – most of whom have trend-following strategies that they employ using very large amounts of money. In another 10 to 20 years, the market might have quite different participants and thus take on a different character.

Any system with a good, positive expectancy generally will improve its performance if more trades are taken in a given period of time. Thus, you can usually improve performance by adding independent markets. In fact, a good system will perform well in many different markets, so adding many markets simply gives you more opportunity.

In addition, performance can usually be improved by adding noncorrelated systems – each with its own unique position-sizing model. For example, if you have a major trend-following system with a very short-term system that takes advantage of consolidating markets, then you’ll probably do very well when you combine them. The hope is that your short-term system will make money when there are no trending markets. This will lessen the impact of any drawdowns produced by the trending system during these periods, or perhaps you might even make money overall. In either case, your performance will be better because you will move into trends with a higher capital base.

14. Mentally plan for worst-case scenario

It’s important to think about what your system could do under a variety of circumstances. How will you expect your system to perform in all types of market conditions – highly volatile markets, consolidating markets, strong trending markets, very thin markets with no interest? You won’t really know what to expect from your system unless you understand how it’s likely to perform under each possible market condition.

Tom Bass was fond of telling students in our system workshop to think about their system this way:

Imagine what it’s like to take the other side of each trade. Pretend you just bought it (instead of sold it) or pretend that you just sold it (instead of bought it). How would you feel? What would your thinking be like?

This exercise is one of the most important exercises you can do. I strongly recommend that you take it seriously.

You also need to plan for every possible catastrophe that might come up. For example, how would your system perform should the market have a 1- or 2-day price shock (that is, a very large move) against you? Think about how you could tolerate an unexpected, once-in-a-lifetime move in the market, like a 500-point drop in the Dow (it has happened twice in 10 years!) or another crude oil disaster as we saw during the Gulf War in Kuwait. Because of the current commodities boom, oil is now as high as $70 per barrel. What if world demand pushes it to $150 per barrel? How will that affect you and your trading? What if we have large inflation again to wipe out our debt? What would happen to your system if currencies were stabilized by linking them to gold and you were a currency trader? Or what if a meteor lands in the middle of the Atlantic and wipes out half of the population of Europe and the United States? Or what about more mundane things such as your communications being shut down or your computers being stolen?

You have to think about what the worst possible scenario could be for your system and how you would handle it. Brainstorm and determine every possible scenario you can think of that would be disastrous for your system. When you have your list of disasters, develop several plans that you can implement for each one. Plan your response in your mind and rehearse them. Once you’ve established your actions in the event of an unexpected calamity, your system is complete.